North Carolina doesn't require SR-22 after most at-fault accidents — only after specific license suspensions involving repeat violations or DWI. Here's when the DMV triggers a filing requirement and what your coverage will cost.

When North Carolina Requires SR-22 After an At-Fault Accident

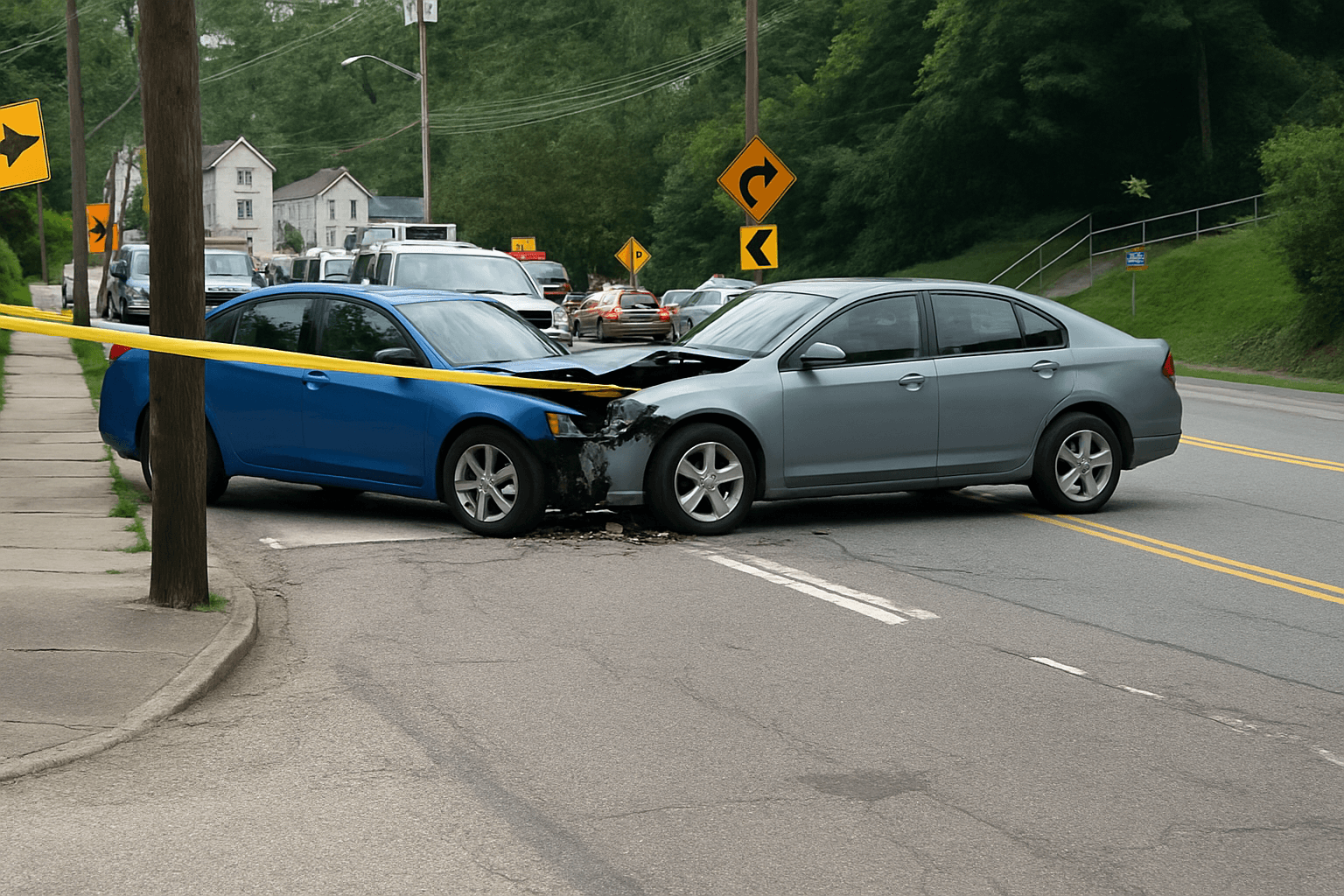

North Carolina does not automatically trigger SR-22 filing after an at-fault accident. The SR-22 requirement comes from license suspension or revocation actions, not the crash itself. If your at-fault accident led to a suspension — for driving without insurance at the time of the crash, accumulating 12 points within three years, or being convicted of a related DWI — then the DMV issues an FS-1 notice requiring SR-22 filing before you can reinstate.

The most common path to SR-22 after an at-fault accident involves uninsured motorist violations. If you caused a crash while driving without insurance, North Carolina suspends your license and registration under the Financial Responsibility Act. Reinstatement requires three years of continuous SR-22 filing. If you had insurance at the time of the accident but your policy lapsed afterward — and the DMV issued a suspension notice for the lapse — you'll need SR-22 for three years starting from your reinstatement date.

Point accumulation also triggers SR-22 in some cases. An at-fault accident resulting in injury or death adds 4 points to your record. If that pushes you to 12 points within three years, the DMV suspends your license for 60 days and may require SR-22 depending on your violation history. Most single at-fault accidents without accompanying violations do not reach this threshold, which is why SR-22 is rarely required from the accident alone. North Carolina SR-22 requirements

What SR-22 Filing Costs in North Carolina

The SR-22 filing fee in North Carolina is typically $25 to $50, a one-time charge your insurer adds when they submit the form to the DMV. This fee is separate from your insurance premium. Some carriers waive the filing fee if you're already insured with them when the SR-22 requirement arrives; others charge the fee at each policy renewal if your three-year filing period spans multiple policy terms.

Your actual cost burden comes from the insurance premium increase, not the filing fee. After an at-fault accident, North Carolina drivers typically see rate increases between 40% and 70% depending on the severity of the crash and whether injuries or property damage exceeded $5,000. If your SR-22 requirement stems from driving without insurance or a DWI conviction — not just the accident — expect increases between 80% and 150%. A driver paying $1,200 per year before an at-fault uninsured accident can expect to pay $2,200 to $3,000 annually once SR-22 is added.

Non-standard carriers often price SR-22 policies more competitively than standard carriers for high-risk drivers. If your standard carrier drops you after the accident or quotes rates above $250 per month, compare quotes from non-standard insurers who specialize in SR-22 filings. Monthly costs for state minimum liability with SR-22 in North Carolina range from $120 to $280 depending on your violation profile and ZIP code.

Find out exactly how long SR-22 is required in your state

How Long You'll Maintain SR-22 Coverage

North Carolina requires three years of continuous SR-22 filing for most suspensions related to at-fault accidents. The clock starts on your reinstatement date, not the date of the accident or the date of suspension. If your license was suspended on June 1 but you didn't reinstate until September 15, your three-year SR-22 period begins September 15 and ends September 14 three years later.

Any lapse in coverage during the three-year period resets the clock. If your policy cancels or lapses for non-payment, your insurer notifies the DMV within 10 days. The DMV suspends your license again, and you must pay a $50 restoration fee plus restart your three-year SR-22 filing period from the new reinstatement date. A single missed payment can add years to your total filing requirement.

Once you complete three years without a lapse, your insurer can remove the SR-22 from your policy. You do not need to file paperwork with the DMV to end the requirement — the DMV tracks your filing period automatically. Your rates will drop once the SR-22 is removed, typically by 10% to 20%, though the at-fault accident will continue affecting your premium until it falls off your driving record after three years from the accident date.

Which Carriers Write SR-22 Policies After At-Fault Accidents in North Carolina

Standard carriers like State Farm, Geico, and Progressive write SR-22 policies for drivers with a single at-fault accident if no other major violations are present. If your SR-22 requirement stems only from the accident and you maintained insurance at the time, expect standard carrier quotes but at significantly higher rates. If the accident involved driving without insurance, a DWI, or multiple violations, most standard carriers will non-renew your policy or decline to quote.

Non-standard carriers dominate the SR-22 market for high-risk drivers in North Carolina. Insurers like The General, Acceptance Insurance, and National General specialize in SR-22 filings and often quote lower premiums than standard carriers for drivers with complicated violation profiles. These carriers accept higher risk pools and price accordingly — your rate may be high, but you'll get coverage when standard carriers won't write you.

Some drivers assume they must stay with the carrier that held their policy at the time of the accident. You can switch carriers anytime during your SR-22 period as long as there is no coverage gap. Your new carrier will file an SR-22 with the DMV when your policy starts, and your old carrier will file an SR-26 cancellation notice. Comparing quotes every six months during your filing period often uncovers better rates as your accident ages and your risk profile improves.

Reinstating Your License After the At-Fault Accident Suspension

Before the DMV will accept your SR-22 filing, you must resolve any outstanding requirements from the suspension. If your license was suspended for driving without insurance, you'll pay a $50 license restoration fee plus any court fines related to the uninsured motorist citation. If the suspension resulted from point accumulation, you may need to complete a driver improvement clinic before reinstatement is allowed.

Once your suspension period ends and all fees are paid, purchase an SR-22 insurance policy. Your insurer files the SR-22 electronically with the DMV, usually within 24 to 48 hours. You can then visit a DMV office or use the online portal to reinstate your license. Bring proof of insurance, your restoration fee payment receipt, and a valid ID. Reinstatement is typically processed the same day if all documents are in order.

Do not drive until your license is fully reinstated and your SR-22 is on file with the DMV. Driving on a suspended license in North Carolina is a Class 1 misdemeanor, punishable by up to 120 days in jail and a mandatory additional year of suspension. Even if your insurer has filed the SR-22, the DMV must process the reinstatement before your driving privileges are restored.

Reducing Your Rate During the SR-22 Filing Period

Your rate won't drop significantly until the at-fault accident falls off your record three years after the crash date. But you can reduce costs incrementally during your SR-22 period by maintaining continuous coverage, comparing quotes, and adjusting coverage limits. Drivers who complete their three-year SR-22 period without any lapses or new violations often see rate reductions of 20% to 30% when the SR-22 is removed.

Switching to a higher deductible or dropping comprehensive and collision coverage can lower your premium if your vehicle is older or paid off. North Carolina requires only liability coverage for SR-22 filing — 30/60/25 minimums — so if you're driving a car worth less than $5,000, consider liability-only coverage. Monthly savings of $40 to $80 are common when dropping full coverage on older vehicles.

Re-shop your policy every six months. Non-standard carriers price risk differently, and the carrier offering the lowest rate at reinstatement may not be the most competitive 18 months later. Drivers who compare quotes twice per year during their SR-22 period save an average of $400 to $700 annually compared to drivers who stay with their initial SR-22 carrier for the full three years.